Does It Actually Matter Who Chairs the Fed?

We got a question recently that we thought was worth addressing publicly. "Should we be worried about the new Fed chair?"

Kevin Warsh officially took over from Jerome Powell on May 22nd. The confirmation was the closest in Fed history, 54 to 45. There was political drama, Senate standoffs, and plenty of strong opinions from all sides. And this morning, May CPI came in at 4.2%, the highest reading since April 2023, which only added more noise to an already loud conversation.

So with all of that as the backdrop, here's our honest take.

The market doesn't really care who chairs the Fed.

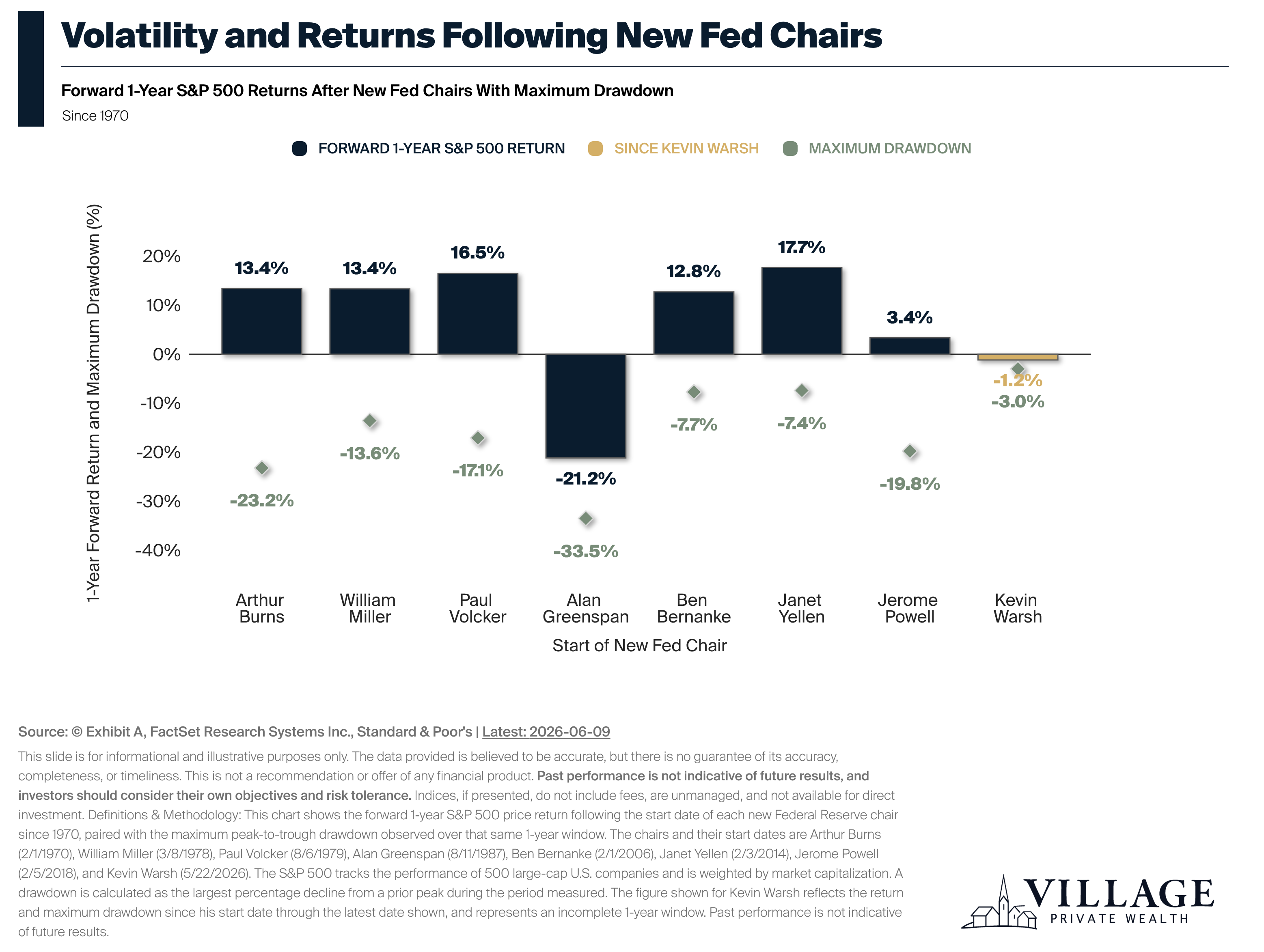

The chart above tracks the forward 1-year S&P 500 return and the maximum drawdown after every new Fed chair since 1970. Eight transitions. Seven completed. The average 1-year return across those seven? Positive 8.0%.

But here's what I think is the more interesting part. Every single one of those transitions came with a significant drawdown along the way. Not some of them. All of them. The average peak to trough drop during those windows was 17.5%. Greenspan's first year saw a drawdown of 33.5% before finishing the year down 21.2%. Paul Volcker's first year had a 17.1% drawdown before recovering and finishing up 16.5%.

The pattern is pretty clear. New Fed chair, expect some bumps. Those bumps don't tell you where things end up.

A lot of those drops had nothing to do with the Fed chair anyway.

Greenspan took over in August 1987. Two months later, Black Monday happened, the largest single day stock market drop in history. That wasn't a Greenspan problem. That was going to happen regardless of who was sitting in that chair.

Bernanke walked into the 2008 financial crisis. The worst economic collapse since the Great Depression. Not a Bernanke story either.

When you see volatility during a leadership change it's easy to connect the dots and assume the chair caused it. But markets are always dealing with something. The person's name on the press release rarely determines the outcome.

One more thing worth knowing about how this actually works.

The Fed chair does not set interest rates alone. The Federal Open Market Committee, which is made up of 12 voting members from across the Federal Reserve system, makes that call by majority vote. The chair leads the conversation. He doesn't control the outcome.

Think of it like the Speaker of the House. Real influence, but not absolute power.

So even with today's hot inflation number adding pressure, and even with Trump publicly pushing for rate cuts, Warsh cannot just decide that on his own. The data and the other 11 voters have a say.

Our take.

New Fed chair, same advice. Stay focused on your goals, not the headlines. The data going back to 1970 shows markets have moved forward through recessions, crises, political chaos, and eight different people in that chair. The name on the door has mattered a lot less than people think.

If you want to talk through what any of this means for your situation specifically, that is exactly what we are here for.